Nigeria’s tax collections have surged by 113 per cent in less than three years, rising from N12.3tn in 2023 to N27.1tn as of July 2026, the Nigeria Revenue Service has said.

The revenue authority attributed the sharp increase to the digitisation of the tax system, the enactment of four new tax reform laws, the transformation of the revenue service and an executive order aimed at closing loopholes in the tax system.

The NRS, in an internal report on the state of the Nigerian economy obtained by The PUNCH on Sunday, insisted that the country was moving from a period of severe macroeconomic distress towards a more stable and resilient economy following the implementation of a series of difficult reforms by the President Bola Tinubu administration.

“Tax collections more than doubled from N12.3tn in 2023 to N27.1tn as of July 2026 with the “digitisation of tax systems, four new tax reform laws, the transformation of the revenue service and an executive order that closed loopholes in the system.

“The Nigerian economy has moved decisively from acute macroeconomic distress toward a more stable and increasingly resilient footing,” the revenue service said.

The NRS attributed the development to what it described as Tinubu’s economic management acumen and determination to implement reforms under his administration’s Renewed Hope Agenda.

According to the report, the administration inherited four major economic distortions which had continued to undermine government revenue and economic growth.

It identified the challenges as “a fiscally unsustainable fuel subsidy regime, an opaque forex system that discouraged investment, a non-performing oil sector, and a tax base ‘far below its potential’.”

The revenue authority said the initial impact of the reforms created significant economic difficulties but maintained that the country’s major economic indicators had subsequently begun to improve.

It cited falling inflation, a turnaround in the balance of payments, increased crude oil production, the emergence of Nigeria as a net exporter of petroleum products and the more than doubling of tax collections as evidence of the recovery.

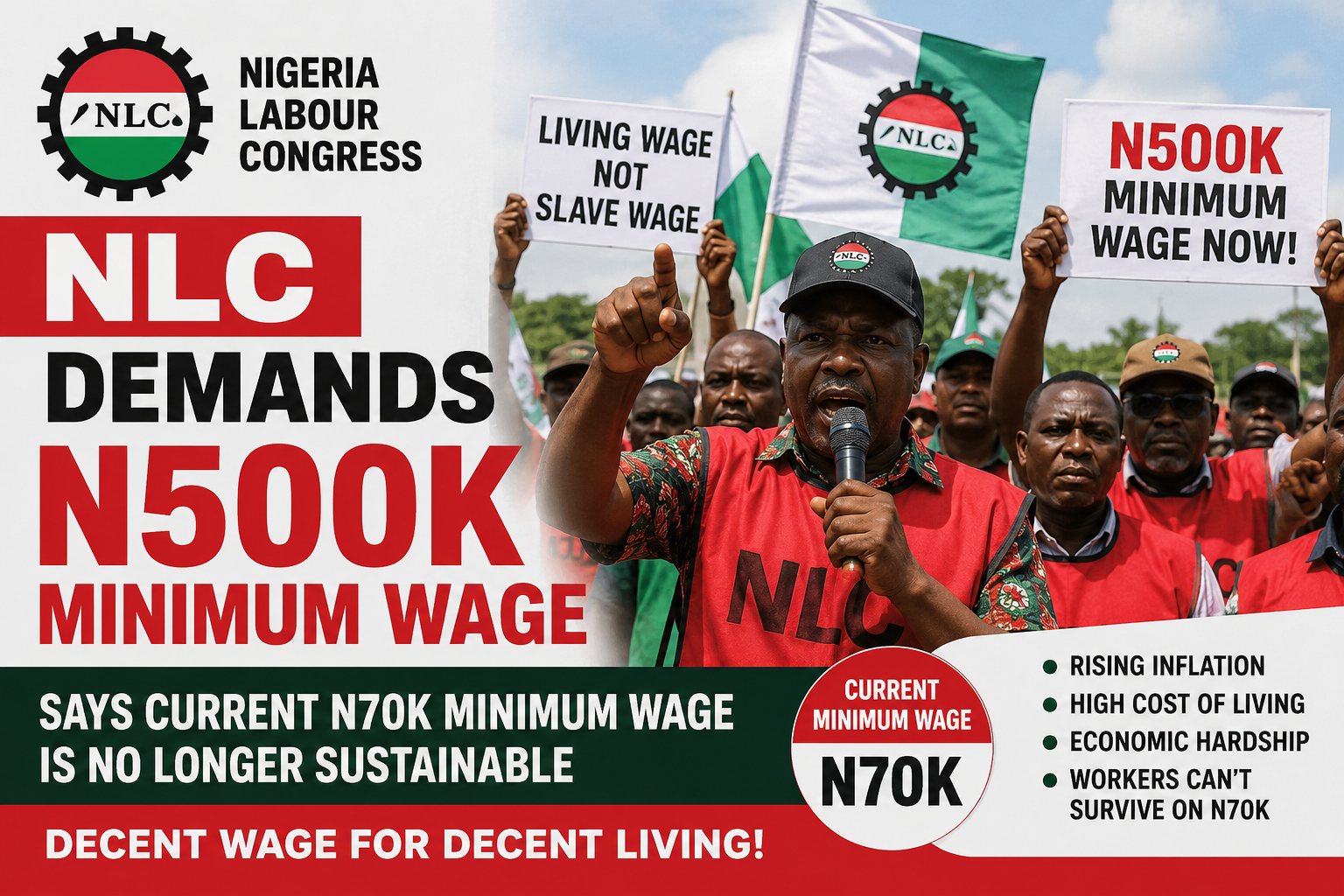

The report also highlighted an increase in the minimum wage, saying it had doubled between 2023 and 2026.

It further cited estimates by the United Nations Children’s Fund showing that the number of out-of-school children had declined from 20 million to 18.3 million following government policies and incentives.

The NRS said the government’s naira-for-crude arrangement with the Dangote Petroleum Refinery and other domestic refineries had contributed to a major shift in Nigeria’s petroleum trade position.

According to the report, the arrangement had helped Nigeria move from being a net importer of petroleum products to becoming a net exporter after decades of dependence on imports.

It noted that Ghana had recently decided to pursue a similar policy in its petroleum sector. The report also said crude oil production had increased from about 1.2 million-1.3 million barrels per day in 2023 to 1.73 million barrels per day by July 2026.

It said the latest output was equivalent to 104 per cent of Nigeria’s OPEC quota. The increase in production is significant for government revenue because crude oil remains the country’s largest source of foreign exchange and a major contributor to public finances.

The NRS also pointed to developments in the capital market as another indication of improving economic confidence. It said the market capitalisation of the Nigerian Exchange had risen from N30.36tn in 2023 to N161tn in 2026, describing the increase as a source of wealth creation for millions of Nigerians who invest in the stock market.

The report attributed the market rally partly to improved macroeconomic credibility, the recapitalisation of banks and a growing pool of domestic institutional investment.

Nigeria’s external reserves also rose sharply during the period under review. According to the NRS report, reserves increased from an unrestricted $3.99bn in 2023 to $51.9bn as of July 2026, which it described as a 17-year high.

The country’s balance of payments also moved from a $3.34bn deficit to a $2.38bn surplus in the first quarter of 2026, the report stated. Nigeria’s trade position similarly recorded a significant improvement, moving from a marginal surplus of N44.7bn to N7.55tn in the first quarter of 2026.

The composition of exports also showed some changes, with exports of other oil products, excluding crude, rising by 51 per cent year-on-year to N6.78tn during the first quarter.

The revenue service said improved investor confidence was also reflected in capital importation. Annual capital importation rose from $3.9bn in 2023 to $23.22bn in 2025, while inflows reached $10.37bn in the first quarter of 2026 alone.

The report said foreign portfolio investment had been particularly strong, while foreign direct investment had also improved. The increase in capital inflows, according to the NRS, reflected stronger investor confidence as economic reforms reshaped the operating environment.

The revenue service further highlighted the expansion of the compressed natural gas programme as part of the government’s response to the removal of the petrol subsidy.

According to the report, Nigeria had no large-scale CNG programme three years ago and depended heavily on imported petrol and diesel. By 2026, however, more than 100,000 vehicles had reportedly been converted to CNG, with more than $2bn in investment mobilised and over 10,000 jobs created.

The NRS estimated that CNG could reduce running costs by between 40 and 60 per cent compared with petrol. It said some commercial drivers had seen their monthly fuel bills fall from about N50,000 to N18,000 after converting their vehicles.

On agriculture and food security, it recalled that the administration declared a state of emergency on food security in July 2023 and subsequently introduced measures including the release of strategic grain reserves, the establishment of a N100bn National Agricultural Development Fund, fertiliser distribution and an agricultural mechanisation programme.

Federal agricultural allocation rose from N228.4bn in 2023 to N826.5bn in the 2025 budget, according to the report. The NRS said food prices had fallen by about 50 per cent by March 2026, citing the Ministry of Agriculture.

However, it acknowledged that agriculture would require several planting seasons before increased government support could translate fully into higher production.

On public debt, the NRS acknowledged that Nigeria’s total debt stock had increased substantially, from N87.4tn in 2023 to N159.28tn in late 2025. However, it argued that the more important measure was the country’s debt relative to the size of its economy.

According to the report, the debt-to-GDP ratio declined from 38 per cent in 2023 to 35.5 per cent in 2025 and 32.3 per cent in 2026. The revenue service described the decline as the first sustained reduction in the ratio in more than a decade.

It also said debt servicing as a proportion of government revenue had declined from 68 per cent to an International Monetary Fund-projected 53 per cent.

The NRS said the combination of higher tax collections, increased oil production, stronger capital inflows, rising reserves and improved trade and balance of payments positions pointed to an economy that was gradually emerging from the severe pressures that followed the government’s early reforms.

The report nevertheless acknowledged that the gains came after what it described as “painful” adjustments and stressed that continued implementation of the reforms would be required to consolidate the recovery.

Source: punchng.com

FOLLOW US ON:

FACEBOOK

TWITTER

PINTEREST

TIKTOK

YOUTUBE

LINKEDIN

INSTAGRAM